SME Interview Kevin O’Brien

Crowdfunding Sources and Proposal: Ulule

Crowdfunding is a relatively new and rapidly growing new segment in the investment community. For the first time, regular people can invest or donate to companies without the need for large amounts of on hand expendable capital. These companies can do this by providing incentives and coordinating large amounts of small donations to reach predetermined and careful considered financial objectives. This has opened the door for a new wave of entrepreneurs that are able to get their idea off the ground and build relationships before the product is even ready to be purchased.

There are three major types of capital that are given out by the project managing team to help get potential clients involved with the brand. These are material rewards, equity and debt. Each has its own advantages and disadvantages. Most crowdfunding websites specialize in a specific type of donation incentive and compensation. Material rewards are the simplest and cheapest for a company to handle. These rewards can range from creative company merchandise or activities to simply acquiring the product before it reaches the mass market. Debt crowdfunding involves using these websites as an alternative to a traditional bank loan. The final alternative is equity which is exchanged for capital.

In the international scene there are several large companies that are connecting entrepreneurs with interested donors. Ulule is a B-Corp certified, French owned crowdfunding website founded in 2010 by Thomas Grange. They use the reward model to provide their donors with unique perks and privileges based on the amount and timing of their donation. Project managers enter the site and establish their desired financial goals. These goals are then examined by a review board that determines whether the campaign’s projections are reasonable and if they are on the correct service. Once the campaign has been approved, donors can begin to send in capital until the project either reaches its goal or doesn’t.

There are two major criteria that the site allows management to use as a scale to judge their success. The first is to set a monetary minimum threshold that must be met. If the camping doesn’t reach its goal, then the money is returned to the donors and no fee is charged. The other metric that can be used is to set a predetermined minimum number of preorders. If a company is selling their product this way, they can avoid the large initial line of credit for their initial inventory. This takes a lot of financial pressure off both the entrepreneur, investors and the management team.

Like all crowdfunding sites, there are two roles that a person can fill when registering for the service. The project creator is the person that establishes the campaign. It is free to register and use the site for anyone over the age of 18. You are also required to have either a European or North American Bank account. Alternatively, donors can be any age and do not require a special bank account. Once the project reaches its set goal, a 5% commission is applied. This only happens if the project has reached its goal successfully. Another important price consideration is the value added tax. This is a consumption tax that is favored over higher income tax in European Union and other places. As a product is processed it increases in value. This additional value is calculated by subtracting the amount already paid towards the product at previous stages in the chain. Many project creators offer material rewards for donating and thus must also consider shipping costs. Ulule offers a service that helps these new entrepreneurs calculate their shipping costs.

How to use the Quick Ratio as a cash management tool

The quick ratio is a financial tool that acts as an indicator of a company’s ability to meet their short-term obligation. These obligations are known as current liabilities and consists of the total amount due to creditors within the next 12 months. This number is compared with the current assets of the company less inventory. Current assets are those that the company is planning on turning into cash within the next 12 months. This ratio can help both investors and entrepreneurs understand and develop a comprehensive cash management strategy. The important thing to remember is that a company that cannot cover its current liabilities with its current assets will most likely need to liquidate alternative assets or raise additional funding. This ratio differs from the current ratio in that it does not include inventory. This is because inventory is not easily liquified.

How to calculate the quick ratio:

(Current Assets-Inventory-prepaid expenses)/Current Liabilities

Or

(Cash & Equivalents + Marketable securities+ Accounts Receivable)/Current Liabilities

Most companies have a Quick ratio of around 1. This means that they have $1 of current assets to cover every $1 of current liabilities. If a company’s Quick ratio is above 1, that means that they have more current assets than current liabilities. Investors often use this ratio to estimate the likelihood of a company losing their investment. If the ratio is significantly higher than 1 it can indicate that the company is not properly allocating its resources. Some companies also choose to hold extra cash on hand to replace the need for outside loans and financing. A low ratio alternatively indicates that the company doesn’t have enough cash on hand to pay for its current liabilities. One common cause of this is a company over reliance on their purchased inventory. If a company is unable to sell the inventory on hand and has a low quick ratio, it is very likely that they will be unable to repay its debts.

Scenario 1

Trail Wizard’s business model is based completely on same day payments. If we were to begin taking money through accounts payable, we wouldn’t be able to restock our inventory or even cover the costs of transportation.

If we were forced to take accounts payable, the first safety blanket we could use is to increase our initial paid in capital. This extra cash on hand can give us room to allow our customers to pay when they can. The other solution is to charge a large late fee that continues to accumulate large amounts of interest daily. This policy is used by rental car locations such as hertz and enterprise. If a person misses the predetermined deadline, a large fee is placed on their account. This can have a large impact on our customer’s interactions and interpretation of our brand. Therefore, any fees would need to be administered by a member of the management team and be clearly communicated.

In this scenario it is very unlikely that my company would survive. With a large amount of our sales tied up in accounts receivable we would need to seek out alternative funds through outside financing. Our business only operates 4 months out of the year so a customer that hasn’t paid would push into our off season.

Scenario 2

My boss at Ramapo Travel Plaza taught us the importance of positive relationships with suppliers. He would always tell us “you pay for what you get, and you get what you pay for”. He believed that it was important to hold our company to the same standard that we hold our suppliers. This means that if a supplier delivers product that is extra or unexpected, that honesty is crucial. We have sent back and even paid for extra product rather than attempt to take advantage of a supplier error. Paying the suppliers on a structured basis is critical for creating that positive dynamic.

In the case of Trail Wizards, these relationships with suppliers will be key. In the hiking community many products are offered only in select stores or locations. This means any inconsistency on our part can lead to a lose of a major competitive advantage that we hope to hold.

Scenario 3

We want to establish a line of credit that can cover a months’ worth of inventory. The goal would be to sell the inventory and then use the subsequent cash to pay back the creditor before placing another order. Around the end of year 3 is where I see the potential for an outside line of credit. With the straight-line depreciation model, our food truck would hit its salvage value and can be replaced. We want to use this chance to purchase a second truck to boost profits. This would require another investment of $21,065. Rather than waiting for the firm to generate the cash needed, we want to use this opportunity to build credit. Our goal would be to repay this loan before the truck depreciates to its salvage value.

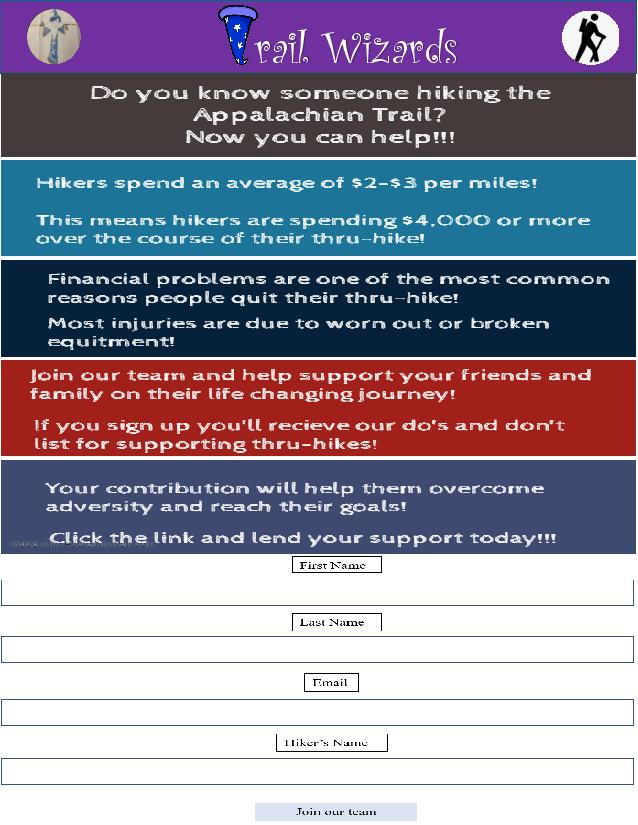

“Two Step” Direct Marketing Tool Write Up

For this assignment I decided to make a response tool targeted towards the family and friends of the hikers. These individuals are back home and watching the progress through social media platforms. This squeeze page will allow our company to begin networking with more than just the hikers themselves. Hiking the Appalachian trail requires an individual to exit society and enter the wilderness. This natural isolation can weigh on a person overtime. That’s why we believe that strong social engagement and support from friends and family back home is essential for a hikers mental and emotional health. We want to encourage people that are already enjoying and liking the photos and videos of hikers to contribute to the trip.

To do this our page is going to offer statistics about the financial hurdles that hikers face.

One of the key statistics we want to use is the amount per mile that hikers spend. Many people back home believe that the hike is cheap because of its separation from society. We want to correct this notion and encourage them to study up and understand all the difficulties their friend or family member is facing. This will become a vital source of support and help to mitigate the financial reasons for coming off trail. It will greatly benefit both our business and the hikers themselves throughout their journey.

After signing up, we want to provide a sheet that offers our advice on how to best lend support to hikers that are out on the trail. This will cover basic information such as common equipment, mistakes and practices of hikers. This information will help them better understand the products and services that we offer and transform a hiker’s solo journey into a collaborative effort with all the support that is required to succeed.

When sending this out to my 5 ideal clients I ran into a delay. I had easy access to the hikers themselves but reaching their family and friends was more difficult. I reached and eventually got 10 direct family members of hikers and 4 close friends from the original 5 hikers. I made age the diverse factor, choosing two hikers over 40 and 3 under 40. The younger hikers had family members view the advertisement and thought that It did a good job explaining the importance of contributing to the hiker’s overall money pool. The older hikers were reluctant to reach out for financial help but that was expected based on the data I had gained during the positioning grid assignment. Overall, the direct marketing tool was a success. Most of the people were asking for more information about how they could contribute and stay up to date on their hiker’s journey. I wanted to keep this information concise so that we could quickly gain the email address before moving into pricing and sales. One late addition based on the feedback from one of the hikers was to include a line where the person could insert their hikers name when signing up. This allows the person to immediately feel as though they are taking this action for them and not for themselves. This actionable advertisement and marketing tool will make it much easier to gather and distribute information in the future. All the names and emails that I gathered through this exercise have also been added to my list of contacts that I’ve already collected. Most of the responses that I gave were very interested in learning more about the day to day experiences of hiking. From my research I have found that many older people were excited just following the experiences of the younger hikers and were excited about the opportunity to help contribute to journeys that are forthcoming. I think that moving forward firsthand written experience and testimony from some of my hiking friends may also become a key resource for drawing clients

SME Interview with Richard Ortiz

SME Interview with Matt Coyne

Supporting and Harvesting

When it comes to the supporting stage of the venture, the understanding of the role that you are to play as an investor becomes paramount. Depending on the specific business and industry, different types of capital need to be administered by the angel or VC. The goal of supporting should always be to help the entrepreneurial venture reach its next value event. According to David Amis, value events include any event that has a fundamental impact on the real or perceived value of a business and its likelihood of success. This means that proper support can help the business scale and attract more investors in later rounds of investment. These events are specific to each business but can more generally be broken down based on industry and stage of development.

An investor coming into a business must make a judgement as to what role they are able and willing to play. Depending on the needs of the business this can be passive with higher financial costs or authoritative with experience driven assistance for the entrepreneur and management team. A silent partner is a type of investor that offers strictly financial investments and allows the management team to run the firm. This takes a large amount of confidence in the team’s ability to navigate the industry and make sound business decisions. A slightly more involved version is the reserve investor. This angel offers a help line for the entrepreneur in the case of unforeseen threats to the business. When called upon the angel can then allocate their time and network resources to the specific issue. The coach investor similarly offers a more hands-off form of an assistance but requires that the entrepreneur provide steady and regular streams of information. This can be a great way to view how the entrepreneur problem solves and deals with adversity without becoming too controlling over daily operations. Team member investors are those that enter the management team and help with the day to day activities. This more hands-on approach gives constant support to the entrepreneur and is more appropriate if the owner is new to the industry and requires consistent guidance. Finally, the controlling investor is one that takes over a majority share in the venture and usually appoints themselves as CEO. This should be done if the angel has little or no faith in the management team or entrepreneur to effectively pursue the opportunity. All these options require varying amounts of resource commitment and should be used in conjunction with your assessment of the context surrounding the business. Time is everyone’s most important resource and must therefore be properly allocated if the venture is to be successful.

During my undergraduate I remember attending an angel event in which startups made visual presentations to potential investors. One business that stood out to me was a new company that developed a technology that replaced oxygen tires with nitrogen. This was shown to increase the fuel efficiency and therefore save on overall expenses. The entrepreneur was convinced that they wanted to take the idea to a broader market and was advised by the potential investors that trucking and shipping fleets would be a better initial public offering for revenue generation. This is a classic example of a conflict in vision by the entrepreneur and potential angel. If a deal was made and the entrepreneur refused to change their mind on their desired market segmentation, then the investor may be required to take a controlling share of the business to guide the firm to profitability. In contrast, if the entrepreneur decided that she is willing to accept the advice of the entrepreneur, then a coaching or reserve role might have been more appropriate. Both the entrepreneur and potential angel want the firm to succeed and these conflicting visions may interfere with the overall profitability of the firm.

During the structuring stage of the investment process, the angel and the entrepreneur should hash out the potential exit strategies to make sure they are on the same page. If supporting goes well, the firm should be on its way towards maximizing its value capturing. When this happens, you must move into the next section of investing, harvesting. In this stage the investor plans to maximize his returns by strategically exiting the firm. There are several ways, both positive and negative, that this can happen. Among the most common are the IPO and the strategic sale of the venture. A strategic sale is when the company is sold to an industry buyer for strategic reasons. These deals are often the most lucrative and quick because they are done by experts within the given industry. The value captured through the acquisition of another venture is determined by factors that often go beyond just the current cashflow of the business. This offers a great opportunity for the investor to get out with insane returns. The concern comes with the potential for the entrepreneur to make deals outside of monetary gains. These deals can shift their decision making and an investor may be unable to affect the outcome. IPO’s on the other hand are simply taking the company public. This allows the management team to continue to run the firm, while also giving the investor a chance at liquidation. A major problem with this method is that it can possibly make the venture more susceptible to threats depending on the market.

As I discussed in previous sections, the relationship is key throughout this entire process. In the early stages we sift through potential ventures and individuals to find attractive opportunities. In the later stages we provide the formalities and the support required for everyone in the situation to benefit. The process is highly reliant on trust and the synchronicity of the management team, angel and entrepreneur. Nobody is a master at investing in the beginning. Through trial and error, you will find which strategies work best for you.

Negotiating

Negotiating is a step that many new angels believe will take up a large chunk of time. This process requires each party to make assertions of their desired terms and find a mutually beneficial agreement. Depending on your level of experience these proceedings can take many forms and can either lead to positive relationships or negative ones. This step should be taken as a chance to build a positive foundation that a future of business dealings and success can be built off.

There are two main schools of thought surrounding negotiations. The first is that negotiations are key to understanding the intentions of the entrepreneur and clearly defining your own part to play in the venture. These people look at the venture’s structure, price, required capital and the role they are expected to play and build the contract around this. The second approach is the avoidance of negotiations all together. This can come in a few different forms but ultimately seeks to save time and avoid putting unnecessary strain on the new relationship. Entrepreneurs in early stage investments are often very emotionally attached to their venture and thus might become defensive or hostile when confronted directly. These negotiations might also take up a significant amount of the investors time that might be better spend pursuing other opportunities or learning about the industry. These entrepreneurs often believe that the price and terms are not significant in the overall scope of the deal.

When it comes to negotiating terms, there are several ways that one can go about it. In the book “Winning angels, the 7 fundamentals of early stage investing”, David Amis suggests 3 methods that are often taken by angels that are seeking to quickly move onto later investment stages. The first of these is the straightforward and direct method. This method calls for active participation and clear language that will lead to either a deal or a clear resolution to the meeting. The most extreme form of this is the one time offer method. This method gives an opportunity for a quick close without the strain that comes from a hostile conversation. This method does place a lot of pressure on the entrepreneur and thus the total scope and context of the deal should be understood before offering. Finally, the negotiation through a third party can be a great method to avoid the time constraints that negotiations can bring. Though many angels chose not to negotiate, those that do are more likely to play an active role in the future of the business.

When considering whether to invest, one should sort out their priorities and decide what they are seeking from the deal. In the case of many investors, the deal itself is less relevant than the potential expansion of one’s network. Respect among the entrepreneur and the investor will help facilitate a positive environment and prevent future snags due to perceived slights. It is important that both the investor and the entrepreneur feel as though they are getting a good deal. Finally, Amis recommends closing the deal quickly. The longer that a deal takes to close, the more likely it is that one or both parties will walk away dissatisfied with the results. Whether you negotiate or not, this stage is key because it is often the first direct interactions between the investor and the entrepreneur. Using the previous steps is key to narrowing down the field but this step is where the future is either build or destroyed. Greed should be discouraged from both parties and these negotiations should be a test run to see whether a business relationship will be sustainable or not.

Structuring

After you have completed the sourcing, evaluation and valuation of the potential investment, you move into the structuring of the potential deal. Depending on what stage or round of investment the startup is in, this may take a few different forms. Just like the previous stages of investment, it is important to remember that this process must be customized to make everyone involved feel comfortable. This process becomes easier with time and angel experience.

In the novel “Winning angels, the 7 fundamentals of early stage investing”, David Amis puts forward three major types of equity that is exchanged for capital in the early rounds of investing. The first of these is common stock. This is the most basic type of stock and comes with the least amount of protection. It is used most commonly in family and friend businesses because it doesn’t require a large amount of time to organize. This stock has no effect on exits from the industry and is only advised if the entrepreneur also holds common stock. Some of the recommendations put forward are the use of tag along rights and preemptive agreements. A pre-emptive agreement gives an early round investor a chance to invest additional capital to prevent a dilution of their equity shares. A tag along prevents the entrepreneur from selling his shares off without also offering the investor an opportunity to exit. Next up is preferred convertible stocks and their terms. These stocks are negotiated with special previsions and offer the investor first rights to the venture’s capital in the event of liquidation. This paired with additional clauses, such as buyout or board seats, give the investor significantly more power in the event of a failure by the management team or entrepreneur. Finally, is the convertible note with various terms. This is a newer model of investment that allows the investor an exit from a failing venture as well as a preferable position on preferred stock later. In this method the investor receives a promissory note that offers a discount based on when the next round of investment takes place. Usually if this round doesn’t take place within a specified period, the investor can receive payment for reimbursement.

No matter which structure you take, the timing of the deal remains an important factor. In early rounds of investing, it can ultimately hurt potential gains if term complexity hinders future rounds of investment. One way to defend against this is by keeping these terms as simple as possible. It is also important to consider whether the valuation on the business is correct. If the first investor overpays, or the management team is undercompensated, motivation may be affected for future contributions.

Ultimately it is important to consider the potential downside that can accompany the mismanaging or judgement of an investment. The first put forward by Amis is the emotional toll from attaching oneself to a failure. For entrepreneurs, failure is part of the growth process and thus is expected. This optimistic mindset is often not shared by investors that haven’t started a venture of their own. The next factor is the financial toll that it can take. Amis suggests that you should never invest more than you are able or willing to lose. Going in over one’s head can lead a person to make decisions emotionally rather than rationally. Finally, the name of the investor may be at risk if the venture doesn’t preform as expected. This can come both from poor financial performance and unethical practices by the management team or entrepreneur. This can damage your network and close future opportunities if not properly managed.